Each era thinks that they had it robust, however proof suggests younger Australians immediately may need a case for saying they’ve drawn the quick straw.

In contrast with younger adults two or three many years in the past, immediately’s 18–35-year-olds might earn extra, however additionally they grapple with hovering dwelling prices, rising training bills, precarious employment and mounting debt.

Shifts within the financial system and labour market have restructured younger maturity, creating new obstacles to monetary safety and delaying milestones akin to residence possession, partnership and parenthood.

How does this examine to what life was like for younger Australians on the flip of the century?

Growing training, reducing payoffs

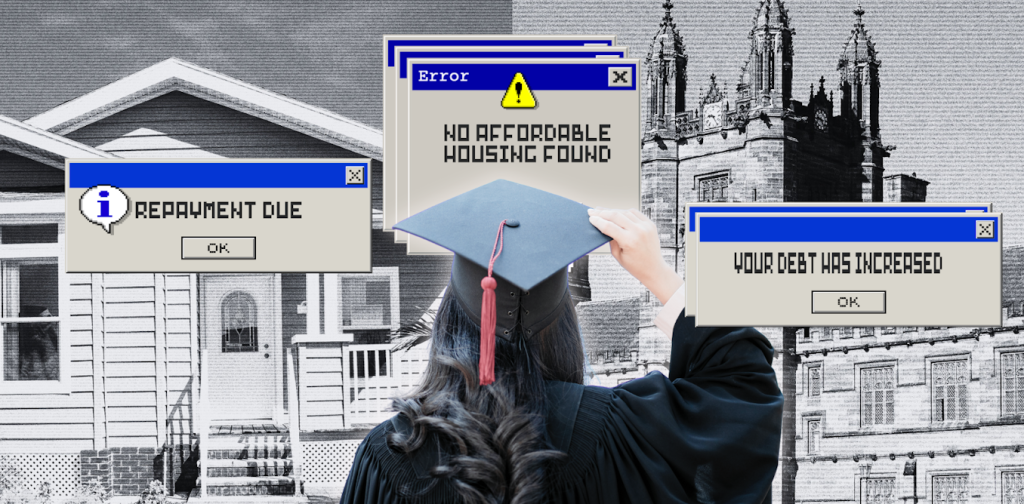

College participation has risen, however so has scholar debt. It’s now far past what was supposed when HECS was launched as a supposedly truthful, income-contingent mortgage system.

Indexation has outpaced wages, a lot in order that immediately’s 20-somethings carry money owed which might be greater than $10,000 larger in actual phrases than their counterparts twenty years in the past.

The Morrison authorities’s 2021 payment hikes solely exacerbated the disaster, with some levels practically doubling in price, leaving college students with a good larger debt burden.

Shutterstock

But the monetary return on training is more and more unsure.

Credential inflation has reshaped the job market, with even low-wage positions now anticipating a college diploma.

The widespread perception {that a} diploma ensures higher pay is driving extra college students into larger training, but there are lots of graduates saddled with debt and dealing in roles unrelated to their {qualifications}.

In 1996, 28.5% of 21–25-year-olds discovered themselves in mismatched jobs.

By 2019, that determine had climbed to 33% simply amongst 25-year-olds.

Salaries aren’t maintaining. Since 1996, graduate wages have risen by an element of simply 2.5, whereas scholar contributions have jumped between 1.7- and 6.2-fold. This leaves immediately’s graduates with debt that consumes a bigger share of their earnings than ever earlier than.

The dwindling dream of residence possession

Housing affordability has collapsed over time.

Twenty-five years in the past, the common home price 9 years’ value of the common family earnings.

Now, it’s about 16.5 years.

In 2001, property costs rose 1.3 occasions quicker than incomes. Since then, they’ve surged at 2.3 occasions the speed.

That is fuelled partly by tax incentive insurance policies – for instance, the Howard authorities’s 1999 capital good points tax modifications – and, extra not too long ago, the COVID pandemic.

Hovering costs have deepened the intergenerational housing wealth hole, decreasing the house buy alternative for younger folks. Whereas the First House Proprietor Grant, launched in 2000, gives some assist, saving for a deposit stays a years-long battle.

That’s, until dad and mom can assist.

For a lot of younger Australians, intergenerational wealth is now the important thing to residence possession. Inheritance is changing into practically as essential as employment.

Since 2002, the overall worth of wealth transfers has greater than doubled in actual phrases, with bigger inheritances anticipated for youthful generations attributable to rising parental wealth and fewer siblings.

However parental wealth is much extra unequally distributed than earnings – formed by training and area.

Subsequently, inheritocracy is ready to deepen financial inequality inside immediately’s youth cohort.

However this isn’t simply in regards to the ultra-wealthy passing down mansions. Most inheritances contain an peculiar residence or proceeds from its sale.

Housing, as soon as central to middle-class stability, now determines who can construct wealth and who will battle financially for all times.

Mounting psychological well being pressures

In the meantime, Australians immediately are borrowing greater than ever. Default danger is rising quickest amongst under-30s as hovering rates of interest, lease hikes, and cost-of-living pressures squeeze funds.

It’s then no shock Gen Z is extra involved about funds than every other era.

Shutterstock

Monetary stress is taking a heavy toll on younger folks’s psychological well being. Between 2007 and 2022, the prevalence of psychological well being problems amongst younger Australians surged by practically 50%.

The burden of illness from non-fatal circumstances – measured in years of wholesome life misplaced – has risen 7% since 2003. That is largely attributable to psychological well being problems and substance abuse, which disproportionately have an effect on younger folks.

Rising up Indigenous

On the deepest finish of those struggles are Indigenous youth, who face far larger challenges than their non-Indigenous friends.

Throughout practically each measure – training, employment, well being and incarceration – outcomes for Aboriginal and Torres Strait Islander younger folks stay considerably worse.

Whereas immediately’s Indigenous youth have achieved higher outcomes in comparison with earlier generations – 39% of Indigenous Australians aged 20+ had accomplished 12 months 12 in 2021, up from 19.4% in 2001 – these good points nonetheless lag behind non-Indigenous youth.

Systemic obstacles, institutional racism and intergenerational trauma proceed to restrict truthful entry to alternatives. This compounds inequalities and contributes to larger charges of psychological ill-health, stress and suicide amongst Indigenous youth.

The altering politics of being younger

Undoubtedly, a continued interval of instability and psychological misery in childhood can be shaping the youngest era’s political attitudes and behaviours.

With fewer property to preserve in comparison with their dad and mom or grandparents, they’re extra more likely to lean extra to the left politically, and this gained’t change with age.

But, they continue to be engaged, thanks partially to obligatory voting, however are additionally abandoning social gathering loyalties.

Australian Election Research knowledge reveals 18–30-year-olds had been extra enthusiastic about politics in 2022 than in 1998 (67% vs 63%). On the identical time, they had been extra more likely to change votes throughout campaigns (43% vs 30%) and fewer more likely to persistently vote for a similar social gathering (28% vs 40%).

Their right-wing identification has practically halved since 1998, with the youth vote more and more favouring left-wing events (75% vs 61%).

Nonetheless, youthful Australians’ various digital information habits add to their political unpredictability. With 60% of Gen Z relying short-form movies, podcasts, and social media platforms for information in 2024, they’re more and more uncovered to fragmented, algorithm-driven content material.

This shift, coupled with rising considerations about misinformation, contributes to their volatility as voters.

Total, younger Australians are coming of age in an period the place arduous work now not ensures safety. How Australia adapts to this shifting financial and political actuality will form the nation’s future for many years to come back.

This piece is a part of a collection on how Australia has modified for the reason that 12 months 2000. You may learn different items within the collection right here.